Navigating the world of tax-advantaged savings accounts like FSA vs HRA vs HSA can feel overwhelming. Each account offers unique benefits and drawbacks, tailored to different financial situations and healthcare needs. Understanding the key differences is crucial to maximizing your savings and minimizing your tax burden. This guide breaks down the specifics of each account, highlighting their features, eligibility requirements, and potential advantages.

We’ll explore the various types of FSAs (healthcare and dependent care), how HRAs work as reimbursement accounts, and the requirements for opening and utilizing an HSA. The comparison table will clarify the nuances between these plans, while the step-by-step guide will help you decide which account best suits your needs.

Introduction to Tax-Advantaged Savings Accounts

Tax-advantaged savings accounts, like FSAs, HSAs, and HRAs, offer a way to save for specific expenses while potentially reducing your tax burden. Understanding the nuances of each plan is crucial for making informed financial decisions. These accounts allow you to set aside pre-tax dollars, which can translate into significant savings over time. However, each account has specific eligibility requirements and usage guidelines, which we’ll explore in detail.

Understanding the Different Plans

FSAs, HSAs, and HRAs each serve a distinct purpose, often overlapping in terms of tax benefits. FSAs are designed for predictable, qualified medical expenses. HSAs are tailored for medical expenses, but also have a broader application for retirement savings. HRAs are typically employer-sponsored accounts for healthcare costs.

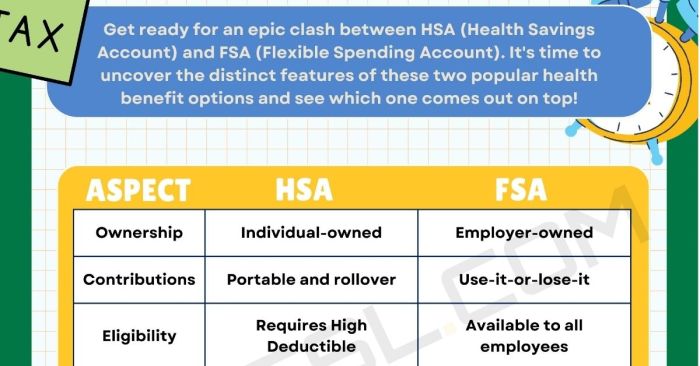

FSA (Flexible Spending Account)

FSAs allow employees to set aside pre-tax dollars to pay for eligible healthcare expenses, including deductibles, co-pays, and some over-the-counter medications. The amount of contributions is determined by the employer, and employees must use the funds within the plan year. They’re generally useful for employees who anticipate relatively predictable healthcare costs.

HSA (Health Savings Account)

HSAs are designed for individuals with high-deductible health plans. They allow pre-tax contributions to cover medical expenses. A key advantage is the potential for tax-free growth and withdrawals for qualified medical expenses. These funds can also be used for retirement, though this may not be the primary function. HSAs are often more advantageous for those with substantial healthcare costs or seeking long-term savings options.

HRA (Health Reimbursement Account)

HRAs are employer-sponsored accounts that reimburse employees for qualified medical expenses. Contributions are made by the employer, and the funds are used to cover healthcare expenses. Often, the reimbursement is tax-free to the employee. HRA plans are typically a benefit offered by employers, and the specific rules are Artikeld by the employer.

Eligibility Criteria and Comparison, Fsa vs hra vs hsa

| Plan Type | Eligibility | Contributions | Tax Implications |

|---|---|---|---|

| FSA | Generally, employees of participating employers are eligible. Specific requirements vary by employer. | Employees contribute pre-tax dollars; contributions are limited. | Contributions are pre-tax, reducing current tax liability. Withdrawals for eligible expenses are tax-free. |

| HSA | Individuals with high-deductible health plans (HDHPs) are eligible. Age and income limits may apply. | Individuals contribute pre-tax dollars; contribution limits vary annually. | Contributions are pre-tax, reducing current tax liability. Withdrawals for eligible expenses are tax-free. |

| HRA | Generally, employees of participating employers are eligible. Specific requirements vary by employer. | Employers contribute; the specific amounts vary by employer. | Reimbursements are typically tax-free to the employee. |

Flexible Spending Accounts (FSA)

Flexible Spending Accounts (FSAs) are pre-tax savings accounts that allow you to set aside money to pay for eligible healthcare and dependent care expenses. By contributing pre-tax dollars, you reduce your taxable income, potentially leading to significant tax savings. Understanding the different types, contribution limits, and eligible expenses is key to maximizing the benefits of an FSA.

Types of FSAs

FSAs are categorized into two primary types: healthcare FSAs and dependent care FSAs. Healthcare FSAs are designed to cover medical expenses not typically reimbursed by insurance, while dependent care FSAs help offset costs associated with caring for qualifying dependents.

Healthcare FSA

A healthcare FSA allows you to pay for certain medical expenses not fully covered by your health insurance. These expenses can include deductibles, co-pays, and even some over-the-counter medications.

Dependent Care FSA

A dependent care FSA helps cover expenses needed to allow you to work or look for work. This often includes daycare, after-school programs, or care for a qualifying dependent who requires assistance to enable you to work.

Pre-Tax Contributions and Take-Home Pay

By contributing to an FSA with pre-tax dollars, you reduce your taxable income. This directly translates to a smaller amount of your paycheck being subject to taxes. Consequently, you will see a noticeable increase in your take-home pay, as less of your income is allocated for taxes. For example, if you contribute $500 per year to a healthcare FSA, that $500 is deducted from your gross paybefore* calculating your tax liability.

This results in lower taxes owed.

Eligible Expenses for Healthcare FSA

Eligible expenses for a healthcare FSA vary but typically include:

- Dental expenses (often not fully covered by insurance): This includes fillings, cleanings, and orthodontia.

- Vision care (glasses or contacts): This includes eye exams, eyeglasses, and contact lenses.

- Over-the-counter medications (in certain cases): Ensure you check your specific plan for allowed expenses.

- Medical equipment or supplies (depending on the plan): This can include things like crutches, braces, or other specialized medical equipment.

Eligible Expenses for Dependent Care FSA

Dependent care expenses eligible for an FSA often include:

- Daycare costs: This covers expenses for childcare that allows you to work or look for work.

- After-school programs: This covers costs for programs that allow you to work or look for work.

- Care for a qualifying dependent who needs assistance to enable you to work: This can cover a range of circumstances, ensuring you have the necessary care for your dependent to allow you to work.

FSA Plan Rules and Restrictions

| Plan Type | Contribution Limits | Eligible Expenses |

|---|---|---|

| Healthcare FSA | Generally $3,050 for 2024 (HSA accounts may have higher contribution limits, depending on the plan). | Medical expenses not fully covered by insurance, including deductibles, co-pays, and certain over-the-counter medications. |

| Dependent Care FSA | Generally $3,050 for 2024 (HSA accounts may have higher contribution limits, depending on the plan). | Daycare, after-school programs, or care for a qualifying dependent to enable you to work or look for work. |

Note: Contribution limits and eligible expenses can vary based on your specific plan. Consult your plan documents for the most accurate and up-to-date information.

Calculating Savings with Pre-Tax Contributions

To illustrate the savings, let’s assume a single person with a 22% tax bracket. If they contribute $500 to a healthcare FSA, they’ll save $110 in taxes (500 x 0.22). This means their after-tax contribution is effectively $390.

Health Reimbursement Accounts (HRA)

Health Reimbursement Accounts (HRAs) are a powerful tool for employees to manage healthcare expenses, often offering significant advantages over other tax-advantaged savings accounts. HRAs work as reimbursement accounts, allowing employees to pay for qualified medical expenses and then be reimbursed by their employer. Understanding how they function, the contribution limits, and tax implications is crucial for making informed decisions about healthcare savings.

How HRAs Function as Reimbursement Accounts

HRAs function as reimbursement accounts, meaning employees pay for qualified medical expenses out-of-pocket and then submit receipts to their employer for reimbursement. This differs from FSAs, where funds are pre-taxed and directly used for qualified medical expenses. With an HRA, employees pay first, then receive reimbursement, often through direct deposit. This structure can provide flexibility in managing medical costs, allowing for the purchase of care at the most opportune moment, as needed.

Contribution Limits and Employer-Funded Contributions

Contribution limits for HRAs vary, and employers are not obligated to fund them. The contribution limits are set annually by the IRS, and employers can choose to contribute to the account, which can significantly impact the benefits for employees. The amounts are typically set by the employer and are a component of employee compensation.

Tax Implications for Employees and Employers

For employees, contributions to an HRA are not tax-deductible, but reimbursements for qualified medical expenses are tax-free. This is a key difference from FSAs, where contributions are pre-taxed. For employers, contributions to the HRA are tax-deductible, reducing their taxable income. This deduction can lead to significant tax savings for the employer.

Key Features of an HRA

| Feature | Contribution Source | Tax Treatment (Employee) | Use of Funds |

|---|---|---|---|

| HRA | Employer (optional), Employee | Contributions not tax-deductible; Reimbursements tax-free | Qualified medical expenses |

The table above summarizes the key features of an HRA. Note the distinct difference in contribution source and tax treatment compared to FSAs.

Key Differences Between an FSA and an HRA

HRAs and Flexible Spending Accounts (FSAs) serve similar purposes but have critical differences in their structure and function. An HRA is a reimbursement account, where employees pay for expenses and are later reimbursed, while an FSA allows employees to pre-pay for qualified medical expenses, reducing their taxable income. The tax treatment of contributions and reimbursements is different in each account type.

This difference in tax treatment and contribution structure often makes HRAs a preferable option for some individuals, as reimbursements are not subject to the same limitations as pre-taxed contributions in FSAs.

Health Savings Accounts (HSA)

Health Savings Accounts (HSAs) offer a unique opportunity to save for future healthcare expenses while enjoying significant tax advantages. They are particularly beneficial for those with high-deductible health plans, allowing individuals to potentially reduce their tax burden and build a substantial healthcare nest egg. HSAs are designed to help manage healthcare costs effectively, particularly for long-term health needs.Eligibility for an HSA is dependent on several factors.

Crucially, individuals must be enrolled in a high-deductible health plan (HDHP) to be eligible for an HSA. These plans typically have a higher deductible than traditional plans but often lower monthly premiums. Furthermore, certain individuals, like those enrolled in Medicare or Medicaid, or those receiving health coverage through their spouse’s employment, may not be eligible for an HSA.

Eligibility Requirements

To participate in an HSA, individuals must meet specific criteria. These requirements include being enrolled in a high-deductible health plan (HDHP) and not receiving coverage through another source, such as a spouse’s plan or Medicare. Additionally, individuals must not be claimed as a dependent on another person’s tax return.

Tax Advantages of HSA Contributions

HSA contributions are tax-deductible, meaning the amount you contribute is subtracted from your gross income before calculating your taxable income. This immediate tax benefit can lead to significant savings on your overall tax liability. Furthermore, distributions from an HSA used for qualified medical expenses are tax-free. This combination of tax deductions and tax-free distributions makes HSAs an attractive option for saving for healthcare costs.

HSAs for Long-Term Healthcare Savings

HSAs are well-suited for long-term healthcare savings. Individuals can contribute annually to their HSA, building a substantial fund over time to cover future medical expenses, such as retirement-related healthcare needs, or potential long-term care expenses. This strategy provides financial security against unexpected or significant healthcare costs that might arise later in life.

HSA Contribution Limits, Tax Deductions, and Potential Penalties

| Feature | Description ||——————-|————————————————————————————————————————————————————————————————————————————————-|| Contribution Limit | The annual contribution limit for HSAs is adjusted annually to reflect inflation.

For 2024, the maximum contribution is $4,150 for self-only coverage and $8,300 for family coverage. || Tax Deductions | Contributions to an HSA are tax-deductible, reducing your taxable income.

This means the money contributed is not taxed. || Potential Penalties| Withdrawing from an HSA for non-qualified medical expenses can lead to penalties and taxes on the withdrawn amount.

These penalties vary, and it is crucial to understand the rules to avoid incurring extra charges. |

Comparing HSA Advantages and Disadvantages for Different Healthcare Needs

| Healthcare Need | HSA Advantages | HSA Disadvantages ||———————–|——————————————————————————————————————————————————————————————————-|—————————————————————————————————————————————————————————————————-|| Routine Healthcare | HSAs can provide a tax-advantaged way to save for routine healthcare expenses, such as annual checkups and preventative care.

| Routine expenses may not always justify the high-deductible plan aspect.

|| Unexpected Illness/Injury | HSAs are beneficial for covering unexpected medical expenses like injuries, illnesses, or surgeries.

The tax-free nature of distributions is a significant advantage. | The high deductible aspect of the HDHP may not be suitable for individuals who anticipate frequent healthcare needs. || Long-Term Care | HSAs can accumulate funds to pay for long-term care expenses, providing financial security in the event of extended healthcare needs.

| HSAs are not designed exclusively for long-term care; other strategies might be necessary for comprehensive coverage.

|

Figuring out FSAs, HRAs, and HSAs can be tricky, right? It’s all about understanding the nuances of tax advantages. Luckily, nets top two powerhouse players talk policy is also discussing important policy points that might impact how these accounts work. Ultimately, choosing the right one depends on your specific needs and financial situation, so it’s always a good idea to do your research.

Hopefully, this helps clear up the differences a bit more!

Choosing the Right Account

Navigating the world of tax-advantaged savings accounts can feel overwhelming. Understanding the nuances of FSAs, HRAs, and HSAs is crucial for maximizing your financial well-being and ensuring you’re making the most of available benefits. This guide will help you decipher the differences and select the account that best aligns with your healthcare needs and financial situation.Choosing the right account requires careful consideration of your individual circumstances.

Factors like your healthcare expenses, income, and overall financial goals play a pivotal role in determining the most beneficial option. This process involves evaluating your healthcare needs and comparing the features of each account to determine which best suits your requirements.

Assessing Your Healthcare Needs

Understanding your healthcare expenses is paramount in choosing the right account. Consider the types of medical care you anticipate needing, including doctor visits, prescriptions, dental care, and vision services. Review your previous medical bills and estimate future healthcare costs to gain a clearer picture of your annual expenditure. This comprehensive assessment will guide you towards an account that covers your expected expenses.

Figuring out FSAs, HRAs, and HSAs can be tricky, but understanding the differences is key for maximizing your benefits. While these plans offer various perks, the latest e-reader market is also heating up, with new Sony devices adding exciting features to the mix. e reader plot thickens with new sony devices are definitely worth checking out if you’re in the market for a new reading companion, but don’t forget to compare the benefits of each plan before making your final FSA/HRA/HSA decision.

Ultimately, knowing which plan suits your needs is essential for smart financial choices.

Evaluating Your Financial Situation

Your financial situation is equally critical. Consider your income, estimated healthcare expenses, and the overall financial benefits each account offers. Evaluate your pre-tax income to determine the potential tax advantages of different accounts. A realistic evaluation of your income and anticipated medical expenses will help you make an informed decision.

Comparing FSA, HRA, and HSA Features

Each account offers unique features. FSAs typically provide pre-tax dollars for healthcare expenses, while HRAs reimburse out-of-pocket medical costs. HSAs, on the other hand, combine tax advantages with the ability to invest funds for future healthcare needs. Understanding the specific features and limitations of each account is crucial in making the right choice.

- Flexible Spending Accounts (FSAs): These accounts allow you to set aside pre-tax dollars for qualified medical expenses. Funds are used to pay for eligible expenses such as doctor visits, prescriptions, and dental care. However, unused funds typically aren’t rolled over to the next year, making FSAs a good choice for individuals with predictable healthcare needs.

- Health Reimbursement Accounts (HRAs): These accounts allow employers to reimburse employees for qualified medical expenses. Often, the employer contributes to the account, and employees use the funds to pay for medical costs. HRAs offer greater flexibility than FSAs, as unused funds can sometimes be rolled over. This is a good choice for those who have unpredictable medical costs or who anticipate needing to use the funds in the future.

- Health Savings Accounts (HSAs): HSAs combine tax advantages with the ability to invest funds for future healthcare needs. Contributions are made with pre-tax dollars, and the account can grow tax-free. HSAs are best suited for individuals with high healthcare costs and a desire to save for future medical expenses. They’re often paired with high-deductible health plans.

Creating a Decision-Making Flowchart

A flowchart can help visualize the decision-making process. Begin by assessing your healthcare needs. Next, evaluate your financial situation. Then, compare the features of FSAs, HRAs, and HSAs. Consider factors like tax implications, contribution limits, and the ability to invest funds.

Based on your assessment, choose the account that best meets your individual requirements.

Figuring out FSAs, HRAs, and HSAs can be tricky, right? Understanding these tax-advantaged accounts is crucial for financial planning. But, what about the cybersecurity challenges in encrypted data, like finding attackers hiding in the shadows? That’s where advanced techniques, like the ones discussed in this article on “smoking out attackers hiding in encrypted data” smoking out attackers hiding in encrypted data , come into play.

Ultimately, securing sensitive financial data, whether it’s in a health savings account or a flexible spending account, requires the same proactive vigilance. So, choosing the right account for you, given the modern threat landscape, becomes even more critical.

| Factor | FSA | HRA | HSA |

|---|---|---|---|

| Tax Implications | Pre-tax contributions | Employer reimbursement | Pre-tax contributions and tax-free growth |

| Contribution Limits | Annual limit | Employer-determined | Annual limit |

| Investment Options | No | No | Yes |

| Account Balance Carryover | Generally no | Potentially yes | Yes |

Implications of Not Choosing the Right Plan

Choosing the wrong account can lead to unnecessary financial burdens. If your healthcare needs exceed the coverage of your selected account, you might face significant out-of-pocket expenses. Conversely, if your chosen account doesn’t align with your financial goals, you could miss out on potential tax savings. Therefore, carefully considering your needs and the features of each account is essential for avoiding these pitfalls.

Plan Administration and Usage

Navigating the specifics of each tax-advantaged account can feel overwhelming. Understanding the procedures for contributions, reimbursements, and tracking your account is crucial for maximizing the benefits and avoiding potential issues. This section will clarify the processes for each account, from initiating contributions to managing your funds.

Contribution Procedures

Understanding how to contribute to each account is vital for proper utilization. FSAs, for example, often have deadlines for contributing, which vary based on the employer’s plan. HRAs, on the other hand, typically have specific contribution limits and may involve employer matching or other incentives. HSAs are set up by the individual, allowing for flexibility in contribution timing.

Claiming Reimbursements or Expenses

Accurate documentation is paramount when seeking reimbursements or claiming expenses. For FSAs, you’ll likely need receipts to support medical or dependent care expenses. HRAs often require similar documentation, but the specific requirements may vary depending on the plan. HSAs, typically used for qualified medical expenses, require detailed receipts and supporting documentation for claims.

Consequences of Non-Compliance

Failure to adhere to the rules and regulations of each account can have serious consequences. For instance, missing deadlines for contributions may result in forfeiting the ability to use the funds for that period. Incorrect or incomplete documentation for reimbursements can delay or deny claims. Strict adherence to each plan’s guidelines ensures proper utilization of the account and avoids penalties.

Claim Submission and Reimbursement Procedures

The process for submitting claims and receiving reimbursements varies across these accounts.

| Account Type | Claim Submission | Reimbursement Process |

|---|---|---|

| FSA | Submit receipts and claim forms to your employer by the specified deadline. | Employer processes the claim and reimburses you directly or issues a payment. |

| HRA | Submit receipts and claim forms to the HRA administrator. | The administrator reviews the claim and either approves or denies it. Payments are typically made directly to the provider or you. |

| HSA | Submit receipts and claim forms to your HSA provider. | The HSA provider processes the claim and reimburses you directly or issues a payment. |

Tracking Account Balance and Transactions

Monitoring your account balance and transactions is essential for effective management. Most accounts provide online portals or statements that allow you to view your contribution history, reimbursements made, and remaining balance. Staying informed about your account activity helps you track your spending and ensure that you’re using the account effectively.

Tax Implications and Considerations: Fsa Vs Hra Vs Hsa

Understanding the tax implications of each account is crucial for maximizing your savings and minimizing your tax burden. Each account offers unique advantages and disadvantages regarding your tax liability, so careful consideration is needed to choose the best option for your individual financial situation. Choosing the right account can significantly impact your overall tax return.Tax benefits and drawbacks vary significantly across these accounts.

Some accounts allow pre-tax contributions, reducing your current tax liability, while others offer tax-free withdrawals for qualified expenses. The potential tax savings depend on your specific income bracket, expenses, and overall financial planning.

Tax Treatment of FSA Contributions

FSAs allow pre-tax contributions, which directly reduce your taxable income. This translates to lower tax payments during the year the contributions are made. However, funds withdrawn from an FSA are not tax-deductible, and you must pay income tax on the amount used for eligible expenses. For example, if you contribute \$1,000 to your FSA, and use \$800 for eligible expenses, you’ll pay income tax on the \$800 when you use it.

The \$200 unused portion of the contribution is forfeited.

Tax Treatment of HRA Contributions

HRAs are funded by your employer and are not funded by employee pre-tax contributions. As such, they don’t directly reduce your taxable income. However, the funds withdrawn for qualified medical expenses are tax-free. This means you won’t pay income tax on the amounts used to cover eligible medical expenses. HRAs are typically funded by your employer, and the tax savings come from the employer’s contribution, not the employee’s.

Tax Treatment of HSA Contributions

HSAs are unique because they allow both pre-tax contributions and tax-free withdrawals for qualified medical expenses. Pre-tax contributions reduce your current tax liability, and withdrawals for qualified medical expenses are completely tax-free. This means you can potentially save on both your current and future tax liability. For instance, if you contribute \$3,000 to your HSA and use it for eligible medical expenses, you’ll avoid paying taxes on that amount.

Tax Implications Comparison Table

| Account Type | Contribution Tax Treatment | Withdrawal Tax Treatment | Tax Benefits | Tax Drawbacks |

|---|---|---|---|---|

| FSA | Pre-tax contributions reduce current tax liability. | Withdrawals for eligible expenses are not tax-deductible. | Lower current tax payments. | Unused contributions are forfeited; income tax on withdrawals. |

| HRA | Employer funded, no employee pre-tax contribution. | Withdrawals for qualified medical expenses are tax-free. | Tax-free withdrawals for medical expenses. | Tax benefits are primarily dependent on employer contribution. |

| HSA | Pre-tax contributions reduce current tax liability. | Withdrawals for qualified medical expenses are tax-free. | Lower current tax payments and tax-free withdrawals. | Account balance is subject to penalties for non-medical withdrawals. |

Tax Form Accounting

Properly accounting for these accounts on your tax forms is essential to avoid errors. Consult with a tax professional or refer to IRS publications for specific instructions and guidance on the appropriate forms and schedules to use for each account. Understanding the nuances of each account and the forms used for reporting is critical to accurate tax filings.

Current Regulations and Updates

Navigating the ever-shifting landscape of tax-advantaged savings accounts can feel like a constant game of catch-up. New legislation, updated guidelines, and fluctuating contribution limits can significantly impact your savings strategies. Staying informed about the latest regulations is crucial for maximizing the benefits of these accounts.

Summary of Recent Regulations

The IRS and relevant government agencies frequently update regulations affecting FSAs, HRAs, and HSAs. These updates can impact eligibility, contribution limits, and the overall usage of these accounts. Understanding these changes is vital for avoiding penalties and ensuring your savings plans remain compliant with current laws.

Changes to Contribution Limits

Contribution limits for tax-advantaged accounts are periodically adjusted to reflect inflation and economic factors. These adjustments can impact how much you can save and the tax benefits you receive. For example, a recent increase in HSA contribution limits could mean you can save more towards retirement and medical expenses, potentially lowering your overall tax burden.

Eligibility Requirements

Eligibility requirements for these accounts can also change. Employers may modify their FSA or HRA offerings, while IRS guidelines on HSA eligibility might shift. Understanding these shifts allows you to assess whether your current plan still aligns with your needs and if you need to explore alternative options. For instance, changes in the definition of “active participation” for a specific employer-sponsored FSA could affect your eligibility to participate.

Potential Impact of New Legislation

New legislation can significantly impact these accounts. For example, a bill affecting the tax treatment of HSA distributions could alter how you approach your retirement savings. The potential impact of such legislation often depends on the specific provisions within the bill, and thorough research is crucial to assess the potential effect on your personal financial situation.

Recent Changes in Regulations (Bulleted List)

- The IRS has updated guidelines on the tax treatment of certain FSA reimbursements, potentially impacting how employees use these accounts for eligible expenses.

- Contribution limits for HSAs were increased for the year 2024, allowing individuals to save more toward future healthcare costs.

- Eligibility criteria for employer-sponsored HRAs have been refined to include specific types of small business owners, potentially expanding access for certain groups.

- The tax code has been adjusted to streamline the process of claiming certain FSA reimbursements, making it easier for taxpayers to track and report their FSA contributions.

Resources for Staying Informed

Staying current on these regulations requires proactive effort. The IRS website, reputable financial publications, and qualified financial advisors are valuable resources. Staying updated through reliable sources can help you make informed decisions about your savings strategies. Reading articles on financial websites and attending workshops on tax-advantaged accounts can provide you with insights into how these changes affect your financial planning.

Ending Remarks

Ultimately, the best choice between FSA, HRA, and HSA depends on your individual circumstances. Consider your healthcare expenses, employer contributions, and tax situation to make an informed decision. This comprehensive guide equips you with the knowledge to select the most beneficial plan, potentially saving you significant money on healthcare costs. Remember to consult with a financial advisor for personalized advice tailored to your specific needs.